How It Works

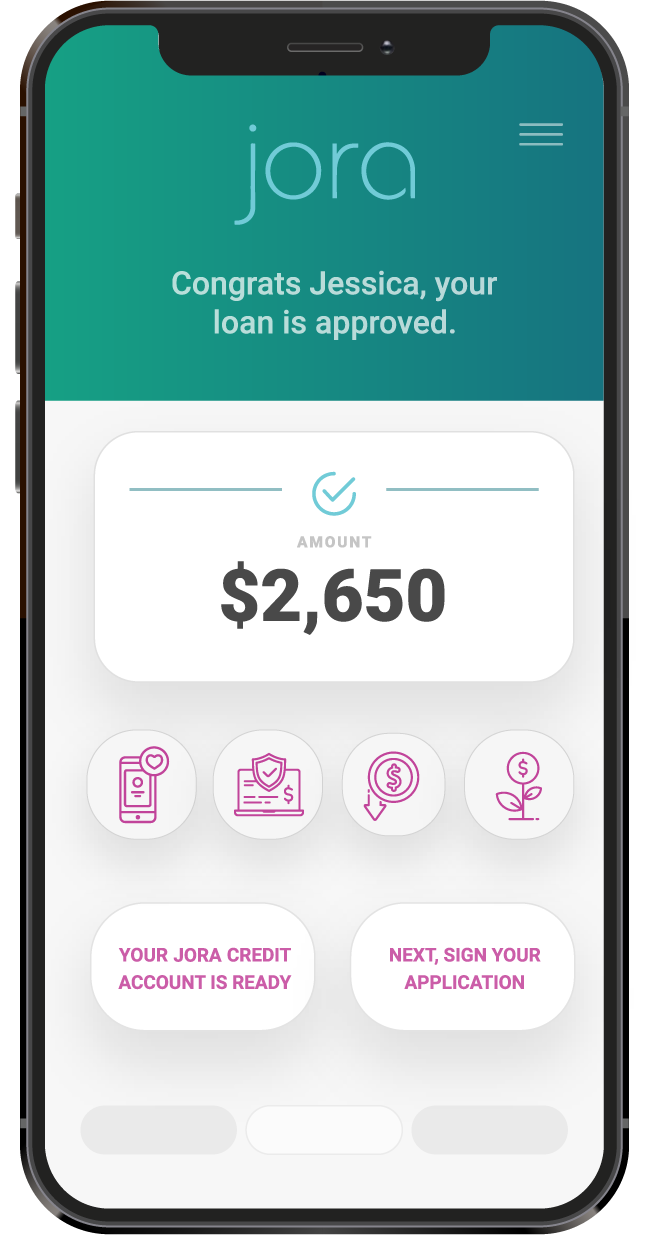

By Applying Online

- Click the Apply Now button below

- Complete application and get a decision within minutes

- Sign your loan agreement and get your money

By Check**

- Sign and complete the back of your check

- Deposit the check in your bank account

- Setup your online account access at myjoraloan.com

Why Jora Credit?

We are a state-licensed, direct lender providing online loans that give you access to the funds you need. And our customers love us. See our Trustpilot reviews below.

Apply in minutes

It’s easy to apply right from your phone, laptop or tablet – anywhere, anytime. And it only takes a couple minutes. Accept your loan by 10:30 am Central time (Monday - Friday excluding holidays) and you can get your funds on the same day.*

Or Deposit a Check

To access your funds, simply complete the back of the check with all required information and deposit it in your bank account. Then, after two business days, go to myjoraloan.com to setup your online access.

Learn more

$5,000,000

Lent

25,000+

Satisfied Customers

15,000+

Repeat Borrowers

Frequently asked questions

Still have a question you need an answer to? Here are the answers to some of our most frequently asked questions.

What financing options are available?

How do installment loans work?

How do lines of credit work?

How often do I have to make payments?

What is the APR on a Jora loan?

What is my borrowing limit?

How quickly will I receive my money?

What is the total cost of a Jora loan?

What is the best way to contact Jora?

Learn More About Online Loans

When it comes to finding the right financing for you, it helps to know all of your options. Here are the main types of online loans to consider.

Read more

© 2017 - 2026 Jora Management, LLC. All Rights Reserved.