Does the Purpose of Your Loan Matter?

Taking out a Loan With Jora

Taking out a loan remains one of the most common ways we finance expensive purchases, significant life expenses, and emergencies. But when it comes to applying for a loan, does the purpose of your loan matter? And do lenders really care how you use the money?

The short answer is yes, but it also depends on what type of loan you take out and the individual lenders' criteria for approving the loan.

Certain loans are designed for specific purchases, whereas others are more flexible. Some lenders limit what you can and can't use a loan for – which could range from strict regulations to more recommended guidelines. For example, lenders may prefer you use a car finance product to buy a car but will also allow you to use a generic personal loan. Lenders always ask about the loan purpose when you apply, so you should be prepared to answer. That answer may or may not impact the lender's decision.

To learn all about using loans for different purposes, keep on reading.

Loans With a Specific Purpose

Some loans are designed to fund particular purchases. In other words, you can only use them for a single, specific thing, not for multiple or diverse purchases. For example, you can't use a student loan to buy a car to travel to college since it's exclusively for studying expenses like tuition and maybe boarding fees.

Lenders offer these car loans specifically to purchase a vehicle. They allow for some flexibility since borrowers can use a car loan for both leasing and purchase agreements. But ultimately, the money must go towards a vehicle.

Car finance typically uses the vehicle as collateral against the loan, making it a secured loan. This means the lender protects themselves if you default on your loan and can no longer repay it.

And because they are usually secured loans, car loans often have more favorable interest rates than flexible, unsecured loans.

While car loans exist, there are alternative ways to finance a car purchase, such as online personal loans. However, car loans might be a better option due to the interest and availability in car dealerships.

For those going to college or who have children going to college, you can take out a student loan to cover the cost of the tuition. Some students opt for federal student loans. However, you can also get private student loans from banks, credit unions, or other lenders.

These loans are intended to help students pay for higher education costs, and so you must use those funds only for that purpose. If a student uses their loan funds for non-education expenses, they may violate the terms of their loan agreement, potentially resulting in penalties or even default.

Mortgage loans are exclusively for purchasing a home, not for other purposes like renovations, investments, or paying off other debts.

When you apply for a mortgage, the funds are disbursed to the seller of the property at closing, and the borrower is then responsible for making regular payments to the lender to repay the loan. The property you buy acts as collateral for the loan if you can't keep up with repayments.

Mortgages can come in fixed-term or variable rates, and because the loan is secured and typically long-term, interest rates are usually lower than other types of loans.

Debt consolidation loans are a type of loan that allows borrowers to combine multiple outstanding debts into one single loan.

The idea behind debt consolidation is that by combining all of a borrower's debts into one loan, they can easily manage their payments and pay off their debts more quickly.

Rather than paying interest on multiple debts, you only make interest payments on one loan, which can save you money. Some lenders specifically offer debt consolidation loan options. Or, you can get a bad credit personal loan to consolidate your debt.

Not all loans have strict usage requirements, meaning you have several options to fund that next big project or trip while meeting your financial goals.

Loans with flexible purposes include online payday, pawn shop, and—the most popular type—personal loans. You can use these for multiple things. For example, if you take out personal loans online, you could use the money for home renovation and a TV upgrade. Or you can cover unexpected legal fees or vacation costs.

Payday loans are a type of short-term loan designed to provide borrowers with quick access to cash in emergencies. These loans are typically for small amounts, usually $500 or less, and borrowers must repay them on their next payday.

Payday loans are a popular bad credit loan option for those struggling to get a loan elsewhere.

A pawn shop loan is a collateralized loan secured by personal property like jewelry, electronics, musical instruments, or other valuable items.

To get a pawn shop loan, a borrower brings their item to a pawn shop where the pawnbroker assesses the value. The pawnbroker then makes a loan offer to the borrower, typically for a fraction of the item's value. The loan amount, interest rate, and repayment terms will vary depending on the pawn shop and the particular item.

The borrower will then leave their item with the pawnbroker as collateral and receive the loan amount in cash. The borrower will have a set period, usually 30-90 days, to repay the loan, plus interest, to get their item back.

If the borrower can't repay the loan within the set period, the item will be forfeited to the pawnbroker, who is free to sell it to recover the loan amount.

Personal loans are a type of unsecured loan that you can use for various purposes like debt consolidation, home improvements, medical expenses, paying taxes, and other unexpected expenses. Banks, credit unions, and online direct lenders offer personal loans—usually without any collateral.

This loan type features set repayment terms and usually lasts between 1-7 years. Borrowers must agree to meet regular bi-weekly or monthly repayments (including interest) until they repay the balance.

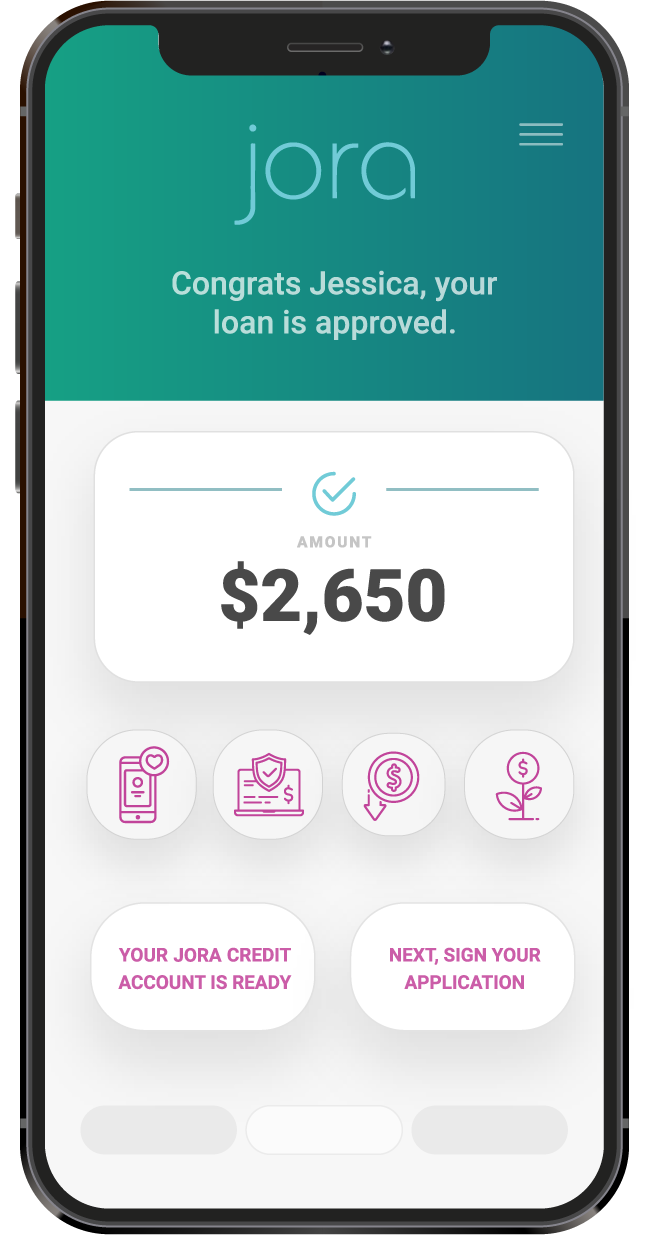

Personal loans can vary greatly in loan amounts, terms, interest rates, and requirements. It all depends on the lender—and the borrower seeking a loan. Some lenders place more emphasis on creditworthiness, but many online lenders offer personal loans for bad credit or even no-credit-check loans. In some cases, lenders hide the additional origination and administration fees and catch borrowers off guard. However, lenders like Jora Credit have no hidden fees to worry about.

In general, you can use personal loans for various things. But there are some prohibited—and frowned-upon—uses.

Each lender will have its own specific rules and restrictions regarding the use of personal loans, so it's crucial borrowers carefully read and understand the loan agreement before accepting the loan.

In some cases, lenders may have strict rules about what you cannot use a loan for – other times they may only be suggestions. For example, lenders may prefer that you use specific loans for things like car finance or educational expenses. But this isn't always a strict requirement.

Whether you get a traditional or online personal loan, here are some common things to avoid paying with loan money.

Most lenders don't allow personal loans to cover tuition costs. The 2008 Higher Education Opportunity Act requires lenders to meet certain criteria to offer a loan for educational purposes. Lenders who do not specialize in educational loans won't meet those requirements, so using their loans for higher education is usually prohibited.

Lenders that offer specific student loans would prefer you use that instead of a personal loan for this same reason. If the lender in question doesn't offer educational loans, your best bet is to find another lender that does.

However, you can use personal loans for other related expenses such as rent, moving expenses, new technology, or equipment. Some educational programs—like tech bootcamps—also accept personal loan payments since they are not traditional higher education options.

Why Jora Credit?

Personal loans are not suitable for home purchases for several reasons.

One reason is that personal loans have much shorter terms than a typical mortgage. In most cases, you would struggle to get a personal loan for longer than seven years, whereas mortgages usually last between 25-35 years because of the larger loan amount.

Taking out a personal loan to fund your down payment is also a bad idea because mortgage lenders won't accept that as a source of funds. Not only does it increase your debt-to-income ratio but also because it signals irresponsible borrowing behavior because you are taking out a loan to take out another loan.

A mortgage is the best method to purchase a home for most people. Mortgages are also secured loans, which means you use the purchased property as collateral against the loan. So if you default on payments, the home is at risk.

However, as a secured loan, the lender's risk is low. So mortgage interest rates are typically lower than they would be with a personal loan. That's why it's usually not worth paying for a home with a personal loan, even if the lender allows it.

The only real exception to this is if you only need a small amount borrowed over a short term to purchase a house in cash. In this case, you won't need to go through the mortgage process. However, this is an unlikely scenario for most, and you may still find that a mortgage is a better option for the reasons above.

In most cases, lenders prefer you to use another type of loan for business purposes. Some may prohibit using personal loans for business, but not all lenders have such strict restrictions.

While it's possible to use the proceeds of a personal loan for business expenses, you should take the time to ask your lender about the terms and conditions of their personal loans.

Many lenders offer different products specifically for business financing, such as business loans, business cash advances, or business credit cards. Those products may offer more favorable terms for business-related expenses, so that may be a better option overall.

Lenders generally don't want to finance gambling-related expenses, so gambling is typically a prohibited use of funds. Gambling presents a high risk for both the borrower and the lender. With risky spending like gambling, there's no guarantee that the borrower will be able to repay the loan, and the risk of default is significantly higher. Lenders also don't want to be associated with potentially illegal activities that might stem from gambling.

Many personal loans' terms and conditions include a clause that prohibits gambling. If you aim to use a personal loan for gambling, you could break the loan's contract and even face legal consequences.

Which is the better loan option for your needs? Perhaps a flexible bad credit online loan? As with lender decisions, this depends entirely on how you want to use the loan. Here are some examples of scenarios and the type of loan that's best suited for each.

If you want to purchase a home or pay for educational expenses, there's a clear winner: opt for the specific mortgage or education loans. These loans will usually offer better loan terms and interest rates, and it will be easier to find a lender willing to accept your application for a loan.

For things like debt consolidation or purchasing a car, the answer is less clear-cut because there are many options available to you. In this case, it's worth weighing up different options and comparing interest rates, loan terms, and individual lender criteria.

If you wish to get fast credit to purchase a big-ticket item or fund ongoing expenses such as home improvement projects, a more flexible option may be a better fit for you. In this case, a personal loan or installment loan online should be able to meet your needs.

The most important thing to do is to look closely at the lenders' restrictions and requirements for each loan product. Compare them to others, and then make a more informed decision that suits your situation best.

Remember that your choice of finance product will also depend on your current income, credit history, debt-to- income ratio, and the desired loan amount.

Credit history, for example, may restrict you from applying for certain loan products or lenders. In this case, you may have to choose a lender that specializes in personal bad credit loans or agree to put up collateral to get approved. Bad credit history may also mean you're unable to get approved for products such as mortgages or car finance.

Frequently asked questions

Still have a question you need an answer to? Here are the answers to some of our most frequently asked questions.

What types of loans does Jora offer?

Who is the lender?

What is required to apply for a loan?

Several types of loans fall under the umbrella term of installment loans, including personal loans and mortgages. An installment loan is where the borrower makes a fixed number of equal payments over a set period. These payments include both principal and interest. The loan's terms, such as the interest rate and length, are agreed upon by the borrower and lender during the loan's origination. The borrower is then responsible for making payments on the loan according to the agreed-upon schedule until the loan is fully repaid.

Jora Credit offers installment loans for bad credit that you can use for various purposes, including home improvements, a vacation, medical expenses, and emergency car repairs.

With Jora Credit, you can get a loan for up to $4,000 in as little time as a few hours, making it ideal for those who need the money in a rush and don't have the best credit history.

With no hidden fees, a quick credit decision process, clear loan terms, and no early repayment penalties, you can get the cash you need fast and clear the loan on your terms.

Learn more about how Jora Credit works or apply online today.